What Senior Living Contract Type Is Best For You, And What Are the Tax Implications?

Choosing a senior living community involves more than selecting a beautiful residence and vibrant lifestyle – it’s also about finding the right financial structure for your future. Understanding senior living contracts and their tax benefits can make all the difference in how you plan for long-term security and peace of mind.

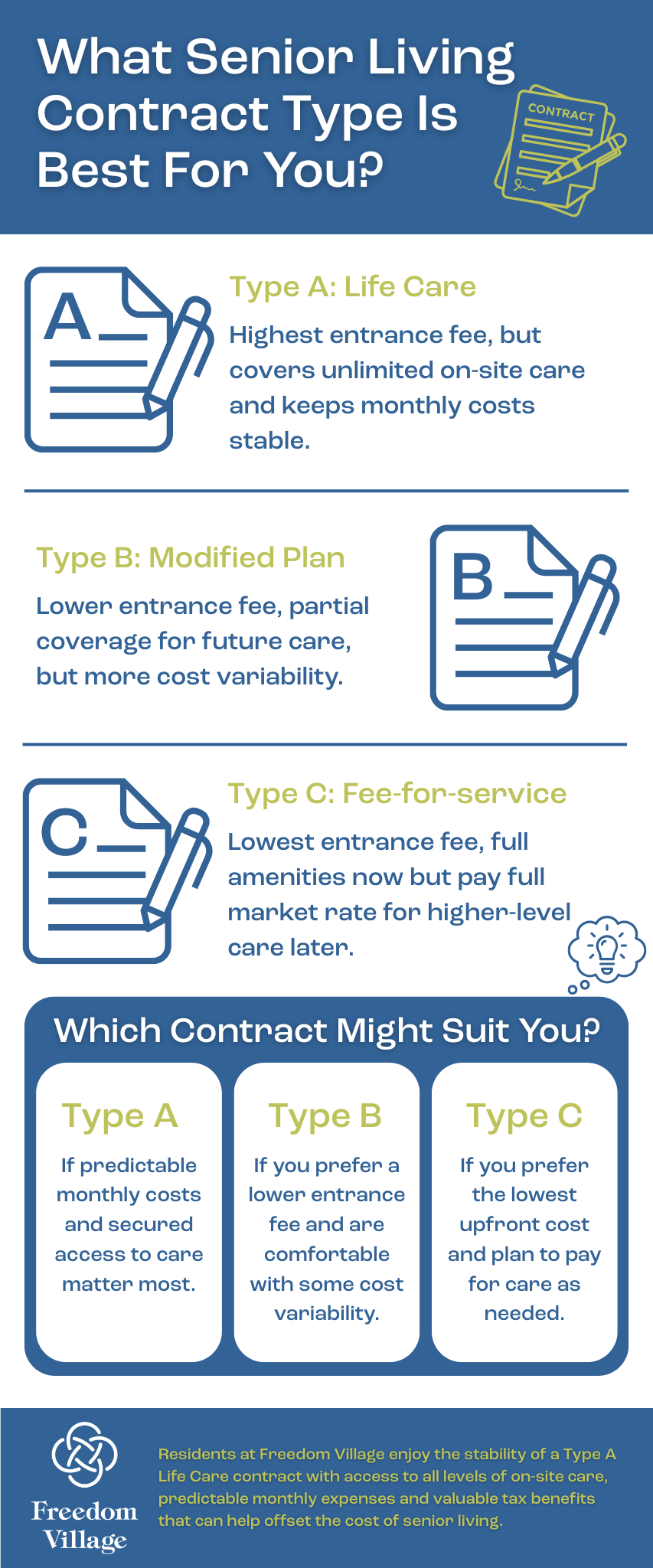

Most Life Plan Communities (also known as Continuing Care Retirement Communities, or CCRCs) offer one of three primary contract types: Type A, Type B, and Type C. Each carries a different balance of risk, reward, and cost predictability – as well as varying potential for tax deductions.

Type A: Life Care – Maximum Predictability and Strongest Tax Benefits

Best for: Seniors who want lifelong security, predictable costs, and the greatest value over time.

A Type A Life Care contract is the most comprehensive option. Residents pay a higher entrance fee upfront, but in exchange, they receive unlimited access to on-site care – including assisted living, memory support, skilled nursing and rehabilitation services – at little or no increase in their monthly fee.

When you consider the ever-rising costs for long-term care on the open market, this model provides a tremendous value with the lowest financial risk and the greatest peace of mind. You know your long-term care is secured, no matter how your health needs evolve. It’s also the contract type with the most significant tax advantages. Because a portion of the entrance fee and monthly service fees are considered prepaid medical expenses, residents may qualify for meaningful tax deductions each year.

To learn more about how these deductions work, see Freedom Village’s guide to the financial benefits of Life Care.

In summary:

- Entrance fee: Higher

- Monthly fee: Predictable

- Financial risk: Low

- Tax benefits: Strongest

Type B: Modified Plan – Partial Coverage, Partial Risk

Best for: Those looking for a balance between lower entry costs and some protection against future care expenses.

A Type B contract typically includes a lower entrance fee than Type A, with partial coverage for future care needs. Residents might receive a preset, limited number of days in a higher level of care at a discounted rate, or pay a reduced fee for services when they need them.

While this middle-ground approach can appear financially appealing, it carries more cost variability over time. If extended care is needed, monthly fees can rise significantly. Additionally, the tax benefits under a Type B contract are usually less because a smaller portion of the fees may qualify as prepaid medical expenses.

In summary:

- Entrance fee: Moderate

- Monthly fee: May increase with care needs

- Financial risk: Moderate

- Tax benefits: Limited

Type C: Fee-for-Service – Lowest Upfront Cost, Highest Long-Term Risk

Best for: Seniors seeking a lowest entry cost and who are comfortable managing potential future expenses independently.

Under a Type C, or Fee-for-Service contract, residents pay a lower entrance fee and enjoy all community activities, services and amenities, plus access to on-site care. However, if higher levels of care are needed, those services are paid for at full market rates.

While this structure minimizes the initial cost of senior living, it carries the highest long-term financial risk – particularly if health needs increase over time. Tax benefits under this model are typically the most limited, as little to none of the entrance or monthly fees are considered medical expenses.

In summary:

- Entrance fee: Lowest

- Monthly fee: Increases with care

- Financial risk: High

- Tax benefits: Minimal

Making the Smartest Financial Choice

While Type B contracts are sometimes marketed as the “smart” financial plan, a Type A Life Care contract offers the strongest overall protection and tax advantages – especially for those who want to age in place and control future costs.

Residents at Freedom Village enjoy the stability of a Type A Life Care contract with access to all levels of on-site care, predictable monthly expenses, and valuable tax benefits that can help offset the cost of senior living. For many, it’s not only the most secure choice – it’s also the most financially wise in the long run.

For a deeper look at how each option compares, visit our blog on senior living contract types or explore current independent living pricing.

Ready to Learn More?

Use our Community Assistant chat feature on this page or schedule a visit to learn more.